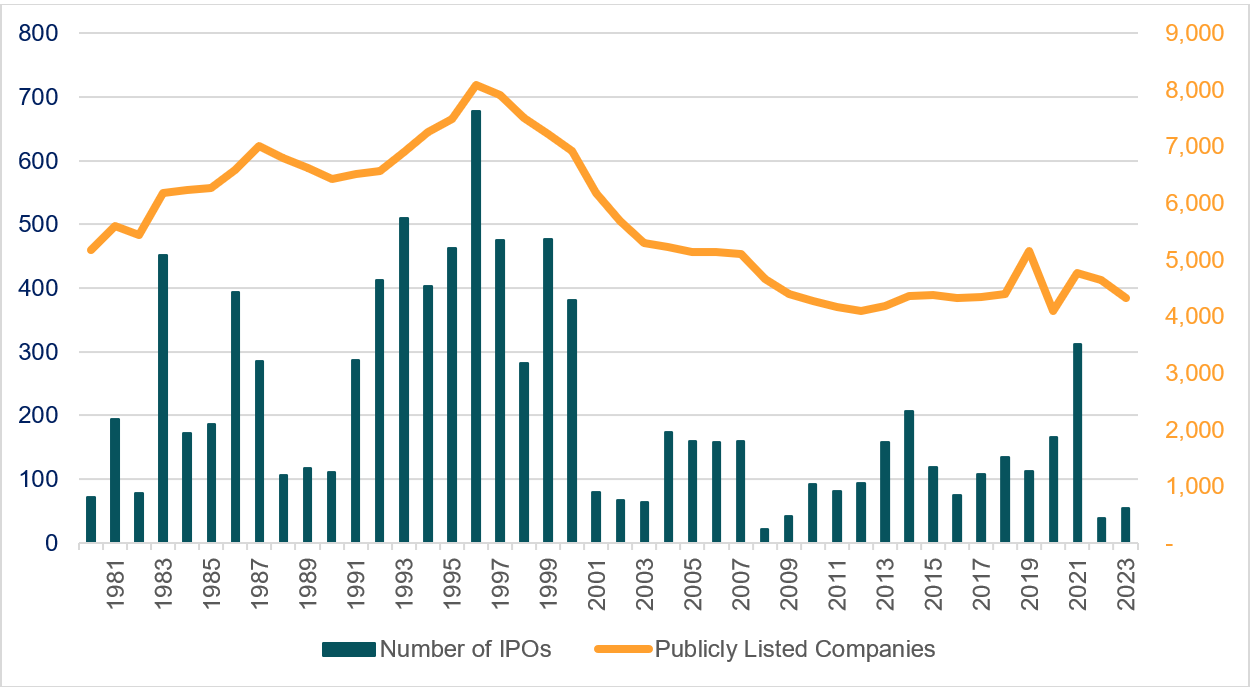

Nov. 14, 2024 – Over the past 25+ years, the number of publicly listed companies on U.S. stock exchanges has fallen sharply. Consider that in the late 1990s, there were more than 8,000 listed companies in the U.S. By 2008, there were less than 5,000. As of 2023, there were approximately 4,317 listed companies.1

Some decline comes from delistings — i.e., public companies that either go out of business or merge with another firm. Private equity firms also acquired some public companies in the period of depressed valuations during the 2022 bear market.2 However, one of the biggest declines is due to reduced IPOs (Initial Public Offerings). In the late 1990s, there were nearly 400 IPOs on average. Fast forward to 2023, there were 54.3 Moreover, many tend to be small deals that don’t raise significant capital. Only ten companies raised $100 million or more in IPO proceeds in the first six months of 2023, compared to 517 such transactions in the same period of 2021.4

IPO Companies vs. Publicly Listed Companies

In 1996, the number of public companies peaked at more than 8,000. Today, there are approximately 47% less.

Source: “Listed Domestic Companies, Total,” World Federation of Exchanges, 2023. Jay Ritter, “Initial Public Offerings: Updated Statistics,” University of Florida, 2023.

It’s helpful for your clients to understand why this trend is occurring, how it might affect their portfolios, and whether they should consider adjusting their investment strategy.