February 18, 2025 – In the past, the traditional private equity (PE) business model could be summed up in two words: leverage and layoffs. Firms financed deals through debt, and they created value in portfolio companies through financial engineering—reducing the size of the workforce and slashing spending. However, the industry has evolved beyond financial engineering in favor of a more holistic approach: improving the operational performance of the companies it invests in.

What’s more, PE managers have a playbook of strategies that they use to create value, tailored to the maturity of the business they’re investing in. For venture and early-stage companies, they often put in capital to help get new ideas to market, and they build up the management team. At the other end of the spectrum are buyout targets, where a PE fund will take over a business that may be in distress and needs restructuring. Between those two poles is a sweet spot for PE: growth-stage companies that hold significant untapped potential. For these companies, PE funds create value opportunities through a strategy of hands-on management. They go under the hood to make a series of operational and financial changes with the goal of unlocking new value.

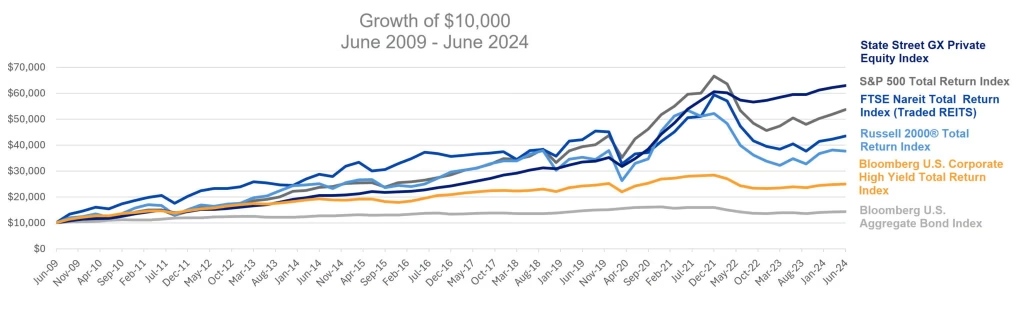

As seen in the chart below, over the long term, private equity has historically outperformed many other asset classes.

For illustrative purposes only and is not intended to represent the results of an actual investment.

The private equity index shown consists of institutional buyout funds, venture capital and private debt, which may be highly leveraged and has high credit risk. The State Street Index above is not a proxy for the private equity asset class. This index displays only a fraction of the global private equity transactions. The benchmark indices are not investments but inform on macro market trends. Past performance is not indicative of future results.

Indices do not address investment costs. You cannot invest directly in an index. There are significant differences between public and private equities, which include, but are not limited to, the following: public equities can provide liquidity and greater access to company information and private equities have a longer time horizon and are considered illiquid. Data represents a variety of broad-based and recognizable indices and is intended to show performance in different asset classes. Risk/reward profile for each asset class varies significantly. SOURCE: Bloomberg and State Street GX Private Equity Index, as of June 30, 2024. (Refer to the dataset information at the end of the article for additional detail.)

In addition, private equity makes up a large and growing slice of the U.S. investment economy: more than $6 trillion assets are controlled by U.S. private equity firms.1 Further, as the total number of public companies has declined; more companies are staying private, meaning that investors may want to consider private equity if they want additional diversification with exposure to a broad set of companies outside of traditional publicly traded markets.2 As investors consider their options, here is an overview of how private equity firms create value.

There are several factors at play. From a high level, private equity funds invest for the long term without having to meet short-term goals such as quarterly earnings targets experienced by publicly traded companies. Private equity firms also have fewer reporting requirements than publicly traded companies. While this can mean less transparency and little to no liquidity compared to publicly traded companies, it can also allow the PE firms to focus more on value creation, operational enhancements and performance management that is less influenced by short-termism. And PE firms tend to be high-performance based, with strong financial incentives for teams to succeed (the management teams that run the companies, not just the PE managers).

For growth-stage companies, a significant way private equity firms can create value is through hands-on management. When institutional investors buy a big stake in a publicly traded company, they meet with management and offer suggestions but don’t have the latitude to make direct changes themselves. Private equity funds, in contrast, can do exactly this—going under the hood to directly change how that company operates. Because they have voting control over the company, they can have a direct say in making improvements.

Operations

- Implementation of lean manufacturing

- Streamlining operations to reduce waste

- Facility evaluation and rationalization to reduce cost

- Automating processes to reduce labor

Revenue Enhancement

- Pricing strategies to reach optimization and increase profitability

- Increased share of customer wallet — same customers, more products/services

- Product line expansion through investment in innovation

- Geographic expansion

- New customer initiatives and diversification into broader end markets

- Sales team expansion/effectiveness

- Optimize commission/incentive structure

Supply Chain

- Identify new vendors, renegotiate prices with existing vendors and create a more competitive marketplace of suppliers

- Reengineer products to reduce costs. Evaluate “make vs. buy” initiatives

- Focus on reduction of ancillary spend — freight, insurance, benefits, etc.

Add-On Acquisitions

- Acquire businesses or products to complement existing offerings and drive increased market share in core markets

- Expand into new and adjacent end markets

- Expand geographically

- Vertical integration

- Revenue and cost synergies

- Conduct acquisitions at accretive valuations — below initial platform valuation/multiple

Some PE offerings are made through a “fund of funds” model, in which they don’t directly manage companies but instead invest in other PE funds. That can work for some investors, but fund of funds managers are one degree removed from the ultimate assets—the portfolio company. The operational improvements we’re discussing in this article come primarily through the direct PE model, where fund managers take direct ownership stake in their portfolio companies and apply a hands-on approach to making operational changes. Because these funds are direct owners of the portfolio company, they have a greater ability to make changes and influence the performance of that company.

To be clear, private equity entails risk like any asset class. Private equity has limited liquidity, higher risks than traditional investments and is not suitable for all investors. But if your clients are even considering private equity, understanding how the model works will help them decide whether it might be right for them.

1 Rebecca Baldridge and Micheal Adams, “10 U.S. Private Equity Firms of 2024,” Forbes Advisor, March 21, 2024.

2 “Listed Domestic Companies, Total,” World Federation of Exchanges, 2023.

Dataset Information

• The State Street Global Exchange Private Equity IndexSM – All Private Equity (GXPEI) is a private equity dataset that includes buyouts (mega, large, mid-size, small), venture capital (early, balanced and late stage) and private debt (distressed, mezzanine, special lendings). Excludes fund-of-funds, secondary funds, alternative investment vehicles, special purpose vehicles and co-investments to avoid double counting. The index is derived from global data of actual cash flows from partnerships held by State Street’s Private Equity Limited Partner (LP) clients and is built using data from State Street’s custodial and administrative services. As of Dec. 31, 2019, the index consisted of over 3,000 unique partnerships exceeding $3.0 trillion in capital commitments representing over 50% of the private equity market. All cash flow data is thoroughly reconciled as part of State Street’s core custodial and administrative services. Because the initial cap index does not depend on voluntary reporting or publicly available information, it is less exposed to biases common to other indices. The end result is an index that reflects consistent and unbiased data, and reliable insight into an otherwise opaque asset class.

• The S&P 500 Total Return Index focuses on the large-cap sector of the public equity market in the United States.

• The FTSE Nareit All Equity real estate investment trust (REIT) Total Return Index is a free-float adjusted, market capitalization-weighted index of U.S. equity traded REITs only. Constituents of the index include all tax-qualified REITs with more than 50% of total assets in qualifying real estate assets. Non-traded REITs are not included in this index.

• The Bloomberg U.S. Aggregate Bond Index measures the investment grade, USD-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, mortgage-backed securities (agency fixed-rate and hybrid adjustable-rate mortgage pass-throughs), asset-backed securities and commercial mortgage-backed securities (agency and non-agency).

• The Bloomberg U.S. Corporate High Yield Total Return Index measures the USD-denominated, high yield, fixed-rate corporate bond market.

• The Russell 2000® Total Return Index measures the performance of about 2,000 small-cap U.S. equities.

• Source: State Street Index and Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Bloomberg does not approve or endorse this material or guarantee the accuracy or completeness of any information herein, nor does Bloomberg make any warranty, express or implied, as to the results to be obtained therefrom, and, to the maximum extent allowed by law, Bloomberg shall not have any liability or responsibility for injury or damages arising in connection therewith.

Represents CNL’s view of the current market environment as of the date appearing in this material only. There can be no assurance that any CNL investment will achieve its objectives or avoid substantial losses. Diversification does not guarantee a profit nor protect against losses.

CSC-1124-3063617-INV